Thailand, Southeast Asia's second-largest economy, is undergoing a healthcare transformation. Population aging, surging medical tourism, and the government's "Medical Economy" strategy are creating significant opportunities for Taiwan's healthcare sector. The key to entry: understanding Thailand's economic fundamentals.

(Image: Canva)

Taiwan’s first two phases of the New Southbound “Healthcare Leads Industries Initiative” have yielded solid results, according to the Ministry of Health and Welfare. Taiwan has secured 39 dental material certifications and 4,957 traditional Chinese medicine registrations, while training 880 psychiatric and mental health professionals from 13 countries across Southeast and South Asia.

As the second-largest economy in ASEAN, Thailand is a strategic center for Taiwan’s medical cooperation network and overseas market expansion. By combining Taiwan’s strengths in healthcare and ICT, Taiwan is positioned to become a key partner in advancing Thailand’s “Thailand 4.0” strategy and “National AI Agenda,” while accelerating the growth of Taiwan’s medical technology and healthcare service exports.

Strategic Position and Current Status of Thailand’s Healthcare Market

Thailand is a key hub in Taiwan’s “New Southbound Policy.” Beyond strong market performance indicators, it has also become a crucial testing ground for Taiwan’s healthcare industry in expanding into overseas markets. According to the World Health Organization (WHO), Thailand’s population is approximately 71.88 million in 2024, with a per capita GDP of US$7,070. However, the income gap remains significant. The population aged 65 and above accounts for 17.5%, while the average life expectancy is 78 years. About 53.5% of Thailand’s population lives in urban areas, compared to 78% in Taiwan, indicating a stronger demand for telemedicine and remote care solutions.

(1) Market Size and Growth Momentum

Thailand’s healthcare market holds a leading position in Southeast Asia and offers a cost advantage compared to Singapore. As a major tourism destination, Thailand hosted over 35 million international visitors in 2024. Combining both domestic residents and inbound travelers, Thailand’s healthcare service coverage effectively reaches a market scale exceeding 100 million people.

The domestic healthcare market alone is projected to reach THB 679.6 billion (approx. US$20 billion) in 2025 and exceed THB 880.5 billion by 2030, representing a compound annual growth rate (CAGR) of around 5.3%.

In terms of medical tourism, Thailand is one of the world’s leading destinations. The medical tourism market was valued at approximately US$2.57 billion in 2023 and is expected to grow at a CAGR of approximately 10.5% through 2030.

Thailand has become increasingly important to Taiwan’s healthcare product export strategy. Taiwan’s medical and health product exports to Thailand grew from US$29.8 million in Q1 2014 to US$51.3 million in Q1 2025. Thailand’s share in Taiwan’s global healthcare product exports reached a record high of 2.62% in Q1 2025. The year-on-year export growth rate was 19.9%, while quarter-on-quarter growth reached 27.1%, signaling rapidly expanding demand.

(2) Industry Structure and Government Strategy

Among Thailand’s medical equipment manufacturers, micro and small enterprises account for 94% of the industry yet contribute only 4.8% of total revenue. In contrast, medium and large enterprises (mostly multinational corporations) represent just 6% of companies but control 95.2% of industry revenue.

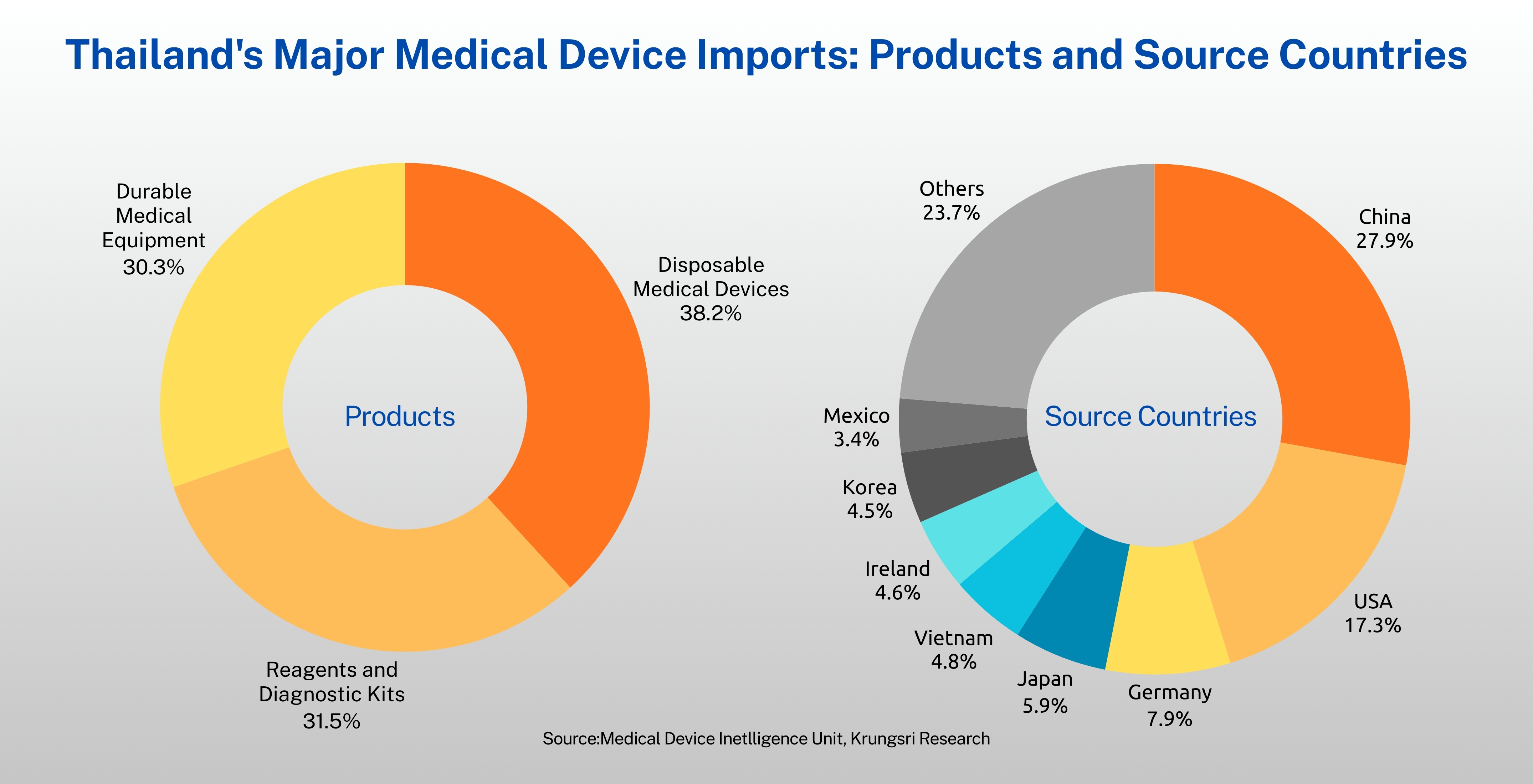

Thailand’s industry is heavily reliant on imported technology and machinery, with local manufacturing dominated by disposable devices. According to the report Thailand’s Medical Device Regulations and Market Entry Strategies, published by Taiwan’s Institute for Biotechnology and Medicine Industries (IBMI), Thailand primarily imports disposable devices, reagents, testing kits, and durable medical equipment. Disposable equipment accounts for 38.2% of imports, while reagents/testing kits and durable medical devices each account for over 30%, respectively.

Together, the top three countries account for 53.1% of Thailand’s total medical device imports. Imported products include ultrasound systems, X-ray machines, ECG devices, diagnostic electronics, ophthalmic equipment, radiology systems, and related machinery.

In September 2016, the Thai government launched a 10-year “International Medical Hub” strategy (2017–2026) as part of its “Thailand 4.0” development vision, aiming to position Thailand as Asia’s medical center. The strategy covers four pillars: medical services, health and wellness, academic research, and product manufacturing. The government further introduced the “Thailand Wellness Corridor (TWC)” to promote healthcare-driven economic development.

In 2021, the government introduced the BCG (Bio-Circular-Green Economy) model to transition Thailand into a high-tech, high-value, and innovation-driven economy. In 2025, the Ministry of Public Health outlined a new “Medical Economy” strategy targeting THB 690 billion in healthcare-related value creation (approx. 3.4% of GDP). Taiwan’s New Southbound healthcare strategy can benefit significantly if aligned with these policy frameworks.

Supply and Demand Landscape in Thailand’s Healthcare Market

(1) Demand Drivers

Key demand drivers include population aging, chronic disease prevalence, medical tourism, and upgrades to the universal healthcare system. By 2030, the proportion of the population aged 65+ will reach 21%. Combined with rising rates of non-communicable diseases, this is boosting demand for long-term and continuous care solutions. Increased public budgets for senior care are supporting corresponding medical device procurement.

Medical tourism and high-income patient segments are driving stable private hospital investment in advanced technologies and premium medical devices. Meanwhile, government efforts to expand universal healthcare coverage will increase demand for basic and widely-used medical equipment in public hospitals.

With over 30 million international visitors annually, Thailand has a solid base for developing medical tourism. (Image: Canva)

(2) Supply-Side Characteristics and Trends

Public hospitals prioritize accessibility and affordability. Their procurement processes are lengthy and heavily constrained by government budgets and specifications, focusing on practicality and durability.

Private hospitals, operating for profit, pursue flexibility, rapid procurement, and differentiation. They emphasize high-end, technologically advanced, and customizable solutions and are more receptive to innovation.

Public teaching hospitals retain strong academic influence, while private hospitals excel in serving high-value medical tourists and high-income patients.

Driven by the “Thailand 4.0” strategy and the national AI agenda, the adoption of AI and digital solutions in medical imaging, hospital management, telemedicine, and predictive analytics is rapidly accelerating—creating favorable conditions for Taiwan’s smart healthcare solutions.

Taiwan, as a global ICT hardware leader, has major OEMs such as Hon Hai (Foxconn), ASUS, Quanta, Compal, Inventec, Delta, and Lite-On forming the AI infrastructure supply backbone. Many of these OEM/ODM companies—along with firms like BenQ Qisda, Biomedica, iMedTec, and V5Med —are already diversifying into medical equipment and telehealth solutions, making them ideal partners in a “Healthcare Leads Industries Initiative” market entry strategy for Thailand.

Additionally, the deployment and operation of AI infrastructure, telehealth systems, and smart medical devices require technical consulting and local staff training. This opens additional service export opportunities for Taiwanese medical institutions.

Key Industry Stakeholders and Certifications

(1) Key Organizations

The Thai Food and Drug Administration (TFDA), under the Ministry of Public Health, oversees medical device registration, licensing, post-market surveillance, and advertising.

The Board of Investment (BOI) provides incentives such as corporate tax exemptions and tariff reductions. High-risk or high-tech medical device manufacturers may receive up to 8 years of corporate income tax exemption.

The Eastern Economic Corridor (EEC) is a major industrial cluster and a priority region for Taiwanese investment. Kinpo Electronics Group has invested in Thailand since 1989, noting advantages such as a stable sociopolitical environment, labor availability, low labor disputes, and reliable energy supply. Delta Electronics and Advantech have also established operations in this region.

(2) Medical Device Regulations and Certifications

Medical devices in Thailand are categorized into four risk classes (low to high). Higher-risk devices require longer approval periods—up to 200–300 days. Foreign manufacturers must register and import through a local distributor. Manufacturers must comply with GMP and ISO 13485 standards. Products already approved by authorities such as the U.S. FDA or EU Notified Bodies may submit simplified documentation to expedite approval.

(Producer: Sophie Y. Wu/Adapted by Judy Lin/Editor: Lihua Wang)

【Deep Read】Targeting Thailand's $20bn Opportunity: "Healthcare-led" Industry Push